Breaking down the J-51 tax abatement: Who is it for, and how can it help?

Skylight explains the tax break that helps New York City apartments recoup costs for building upgrades

A demonstrator holds a sign at a rally to support the continuation of the J-51 tax break. Photo: Hannah Berman

New York City property owners know that renovations can be a headache. They are usually costly, chaotic, disruptive, and they tend to take longer than expected to complete. But they’re a necessary part of building upkeep, and now, they’re a crucial part of helping buildings comply with the city’s commitment to reduce carbon emissions from its built environment.

The J‑51 tax abatement program exists to offer building owners a break on their tax bill to offset the cost of those frustrating upgrades and repairs. The rationale behind it is as simple as it sounds: If renovating a building leads to substantial tax cuts, owners are more likely to take on that renovation.

The law was first introduced in 1955 to help New Yorkers take care of the city’s many crumbling buildings, and has since undergone many updates and controversies. The latest iteration of J‑51 was created in 2023, when Governor Kathy Hochul signed it back into New York State law, with the final city rules released in June 2025. The revived tax abatement was hailed as a way to meet the challenge of climate change and help buildings comply with Local Law 97 (LL97), providing some financial support for substantial renovations like boiler upgrades, heat pump installations, or other interventions to adapt building energy consumption to the new standards.

Yet now that J‑51 is back in place, already the clock is ticking — the tax break only applies to projects completed by June 30, 2026, leaving property owners an extremely tight window to get work done. This could change, however, due in no small part to the groups of New York City property owners lobbying the state for an extension commensurate with LL97’s aggressive clean energy timeline, and changes to the law that would make it accessible to more buildings. As the future of J‑51 continues to evolve, refer back to this page for updates.

In the meantime, here are the basics that every New York City property owner should know.

New York City Councilmember Erik Bottcher speaks in support of the J-51 tax abatement at a Green Co-op Council campaign launch. Photo: Hannah Berman

What is the J‑51 incentive?

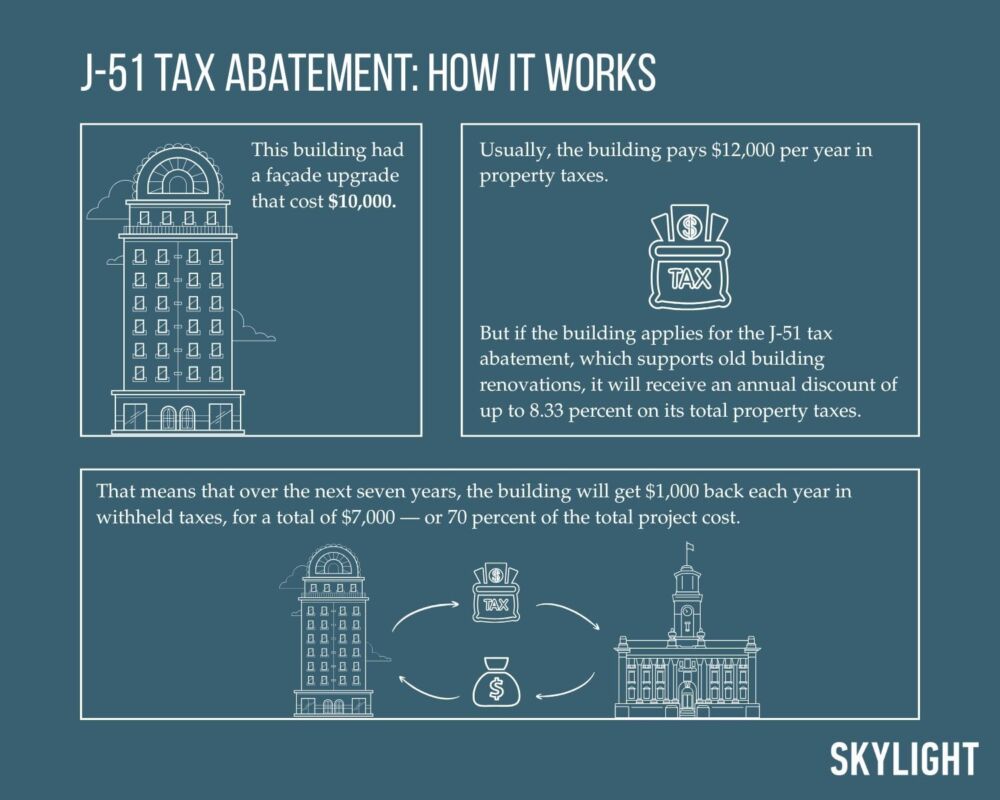

The J‑51 incentive is a tax abatement, or exemption, that temporarily reduces or eliminates property taxes for buildings that undergo renovations. It offers an abatement of up to 8.33 percent of total real estate taxes for up to 20 years, until the total abatement covers up to 70 percent of the total improvement cost, provided the work meets reasonable cost caps — more on that below. After that, a building’s owner goes back to paying full real estate taxes based on the current value of the building.

For example, if a building has eligible work done for $10,000, it can get up to $7,000 back in real estate taxes over 20 years, by getting a discount of 8.33 percent of the total taxes until the discount reaches $7,000. So if the real estate taxes on that building would be $12,000 a year, an 8.33 percent discount amounts to $1,000 a year. In seven years, the building’s abatement will be covered — and in sum, the renovations will have cost $3,000, or just 30 percent of sticker price.

How the J-51 tax abatement works.

J‑51 benefits are stackable: if a building is still benefiting from an abatement for past improvements, a new eligible improvement will add an extra abatement. That same building could conceivably take on several other projects and receive more money back overall.

To understand the full scale of the J‑51 benefit, property owners should keep in mind both the cost of a proposed project, and the size of their overall tax bill. Property taxes are calculated based on a building’s assessment, or its value as established by the New York City Department of Finance (DOF). Every January, the DOF mails a Notice of Property Value (NOPV) to owners, informing them of the assessed value of their property for the year. The assessment is a percentage of the NOPV, which changes depending on the type of real estate. For instance, the assessed value of co-ops and condos is typically 45 percent of the market value, or the income potential for that property. For smaller, one- to three-unit properties, the assessed value is much lower, at 6 percent. The city publishes all property assessments yearly.

What work is covered by J‑51?

The broader framing of the J‑51 incentive is the same as previous iterations, covering major capital interventions, such as a new roof or a façade repair, and conversions from non-residential into multiple dwellings. The 2023 version of the incentive, however, also covers the kind of work necessary to abide by LL97 requirements, geared toward energy efficiency.

To be eligible for the abatements, the interventions need to meet a minimum cost of $1,500 per dwelling, and the cost has to be below the caps set for each type of intervention on the city’s Certified Reasonable Cost Schedule — for instance, asbestos abatement has to cost $22.23 or less per square foot to access the tax break. Owners facing work that falls on the lower end of the cost spectrum may not find the incentive worth their time and investment, said Priya Mulgaonkar, director of the Green Co-op Council, when they account for the fees and specialized help necessary to complete the process.

What buildings are covered by J‑51?

The current J‑51 incentive focuses specifically on affordable housing. Buildings are eligible if they fall into one of these four groups:

- Buildings where the average assessed value (see above for how this is determined) of each unit is under $45,000;

- Buildings where at least half the apartments are designated affordable (as in, rented exclusively to families making 80 percent of the average median income);

- Buildings that are operated by limited-profit housing companies (established specifically to build affordable homes);

- Buildings that receive substantial government assistance.

Overall, according to the NYC Department of Housing Preservation and Development (HPD), which administers the program with the NYC Department of Finance, about 700,000 units are eligible, or about 20 percent of the city’s total housing stock. The full list of eligible buildings, organized by neighborhood, is available here.

There is also a key provision for rent stabilized tenants. Previous versions of the law allowed landlords to pass the costs of renovations onto their rent-stabilized tenants, even if they were claiming the tax abatement. In order to benefit from the abatement, a landlord needs to absorb the remaining 30 percent, and is not allowed to pass it on under the guise of capital improvement.

How does the J‑51 abatement application work?

There are several sets of forms and documents to file, both before and after the work is completed, in order to get the J‑51 abatement.

Prior to the beginning of the work, owners have to file:

- A notice of intent;

- A notice to tenants (to be given between 30 and 180 days prior to the start of the work); and

- An affidavit confirming the notice to tenants.

Delays in filing a notice of intent are subject to a penalty of $500 or 10 percent of the application fee, whichever is greater.

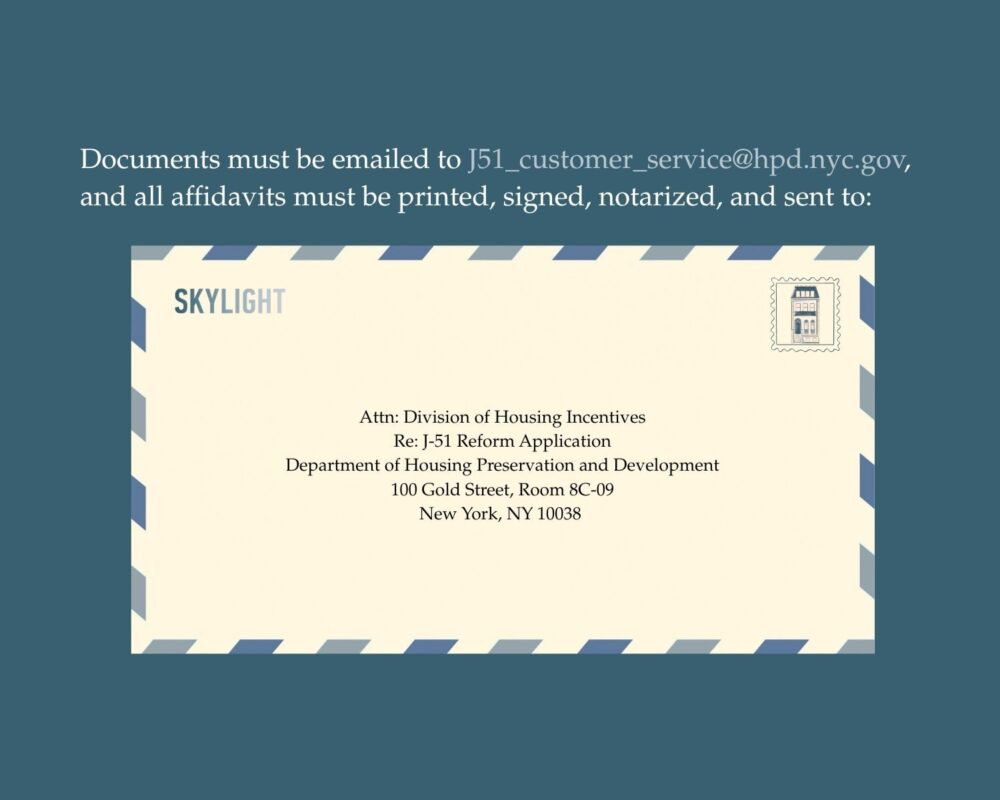

After the work is complete, the order of operations goes like this: Owners must file an application and application fee (more on that below), and a building addendum if the block and lot have more than four buildings. A long list of other documents and affidavits (up to 24 total for rental buildings and homeowner buildings) has to be included with the application, including an excel workbook, a proof of eligible costs, and a certificate of compliance with DOB regulations. The full list of required paperwork is here.

The application documents must then be emailed to HPD, but note that all affidavits must be printed, signed, notarized, and sent via mail to this address:

How to apply for the J-51 tax abatement.

Application fees must be filed after the work has been completed. The base J‑51 application costs $1,000 for buildings with up to six units. Buildings with more than six units must pay $75 per additional unit. For small buildings, this doesn’t make much of a difference — in a ten-unit building, for example, the total application cost would be $1,300 — but for larger buildings, that extra per-unit cost can really add up. In a 500-unit building like the Victoria in Union Square, just applying for the J‑51 abatement would cost almost $40,000, on top of the cost of renovations.

This extra cost, along with the complex application process, is part of what advocates for co-op and condo owners see as the problem with the existing legislation. “Every program and incentive… for Local Law 97 has its own red tape,” said Mulgaonkar. “They kind of compound on each other… and become burdensome.”

When do I have to submit my J‑51 application?

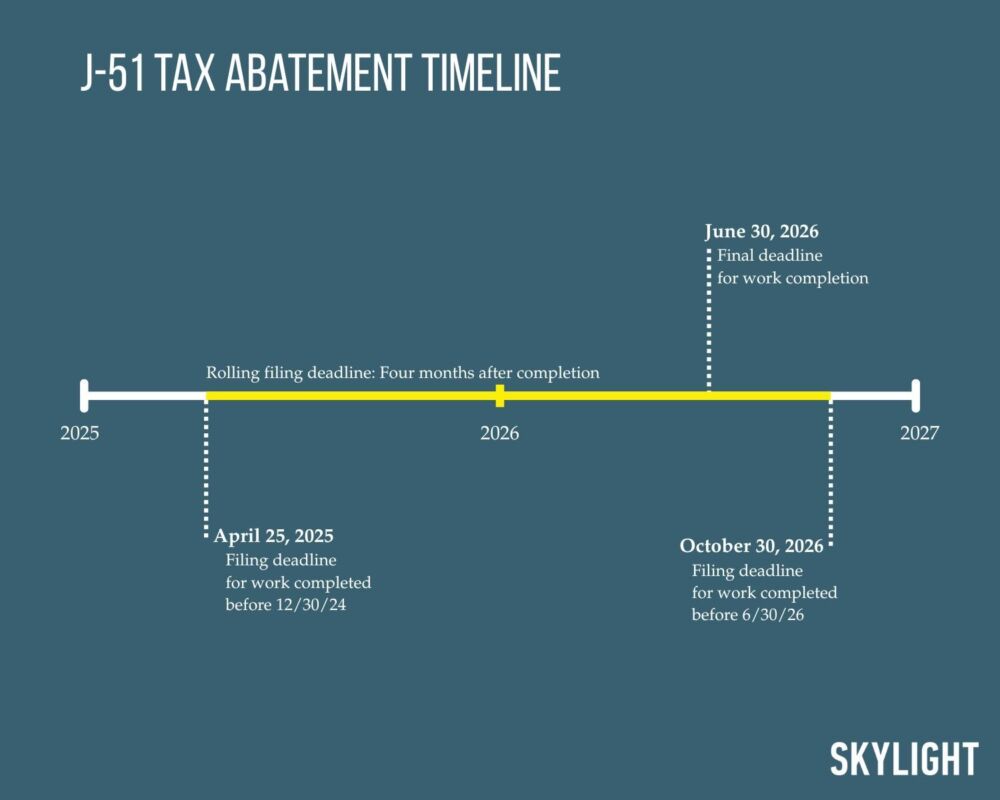

Arguably the biggest challenge for property owners looking to benefit from this current iteration of J‑51 is its timeline. The incentive applies to building renovations completed after June 29, 2022 and before June 30, 2026, and cannot take more than 30 months from beginning to completion. For work that was completed some time ago, the deadline to submit has already passed; abatements for all work completed before December 30, 2024 had to be filed by April 25, 2025. For work completed after December 30, 2024, property owners must file for the abatement four months after completion.

Past and upcoming dates to note for the J-51 tax abatement.

For anyone considering undertaking a project that they want offset by J‑51, it’s important to remember that the abatement can only be claimed once the work is completed, which means owners have just over a year left to complete renovations in order to qualify — even though the rules were only finalized this past summer.

Because of this, as well as the lack of awareness about the renewal of the program, there aren’t many buildings that have been able to claim the abatement so far. Condo and co-op advocacy groups are now mobilizing to ask lawmakers to extend the deadline until 2030 to go hand in hand with LL97 deadlines, a move that incoming New York City mayor Zohran Mamadani supports. For now, the recommendation from experts is that buildings should secure financing, find a contractor, and get the work started, aiming for completion in June 2026, so as to have extra time in case of delays and to apply for the abatement.